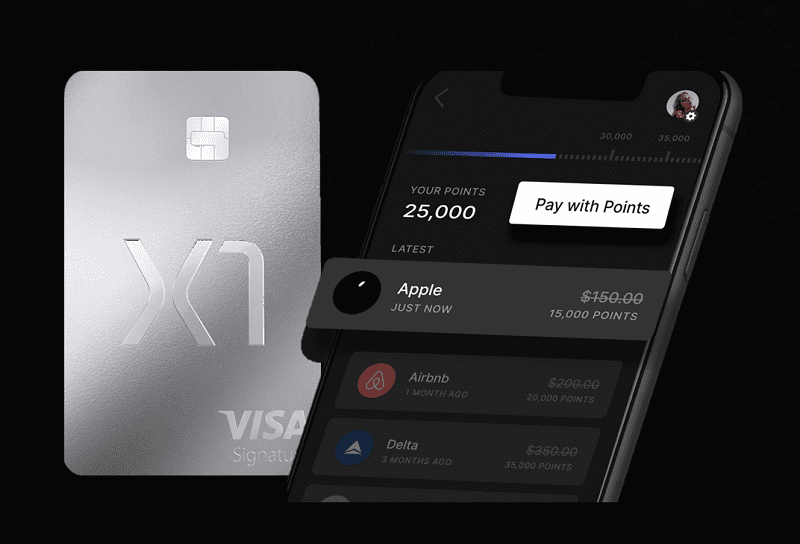

The X1 Card is now available to everyone without a waiting list.

The Capital One Venture X isn't the same as the X1 card.

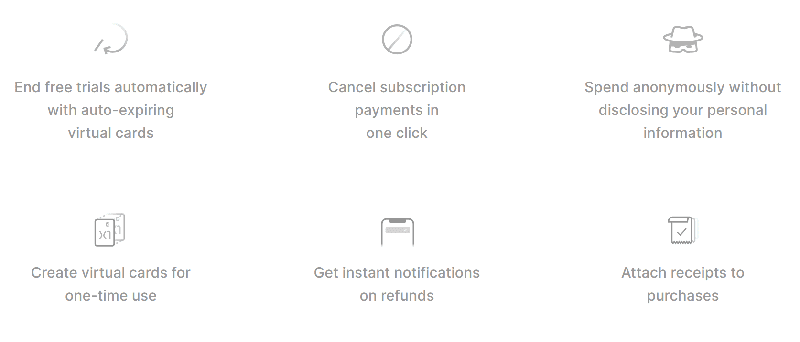

The X1 card earns 2x, 3x, or 4x for all spend and has no fees. It also offers cool features like auto-expiring virtual cards so that you can sign up for free trials without any risk of being charged if you forget to cancel.

The only way to get the card was through a referral.

X1 Overview

The X1 Card has an overview on it.

iPhone or Android: When X1 first came out it was only available for iPhone users, but it is now available for Android users as well.

Heavy metal: 17g “Pure Stainless Steel”

Card network: Visa Signature

Earn 2x to 3x everywhere: Earn 3x if you spend over $15K in a year (otherwise 2x);

Earn up to 5x with boosts: Earn up to 5x with various “Boosts”

Earn more with referrals: Earn a mystery reward when a friend signs up with your link: 4x, 5x, or 10x.

Annual Fee: $0

Late Fee: $0 (but you will be charged interest on the balance of course)

Foreign Transaction Fees: $0

Welcome bonus: Earn a mystery bonus for the first 30 days by signing up using a friend’s referral code. Earn 4x, 5x, or even 10x.

Virtual card numbers: Easily create virtual card numbers in the X1 app with several options:

Singe-Use Card: Auto-cancelled after 1 purchase

Free Trial Card: Auto-cancelled in 24 hours

Standard Virtual Card: Cancellable at any time.

Advanced:

Optionally set a monthly limit

Make the card Anonymous

Auto cancel: Never; after 1 day; after 7 days; after 30 days

Higher credit limits: My X1 card has a $30K limit which is considerably higher than most of my other cards.

No hard credit inquiry: X1 does a “soft pull” of your credit (Note: one reader says that they issued a hard pull so YMMV).

Benefits:

Purchase Security: 90 day protection from theft or damage

Extended Warranty Protection: Double warranty, up to 1 extra year

Return Protection: Up to $250

Cell Phone Protection: Max $500 per claim, $50 deductible. Requires paying your monthly cell phone bill with the card.

Trip Interruption or Cancellation: Up to $2,000 per person.

Auto Rental Collision Damage Waiver: Secondary. No coverage in Israel, Jamaica, the Republic of Ireland, or Northern Ireland.

X1 adds to your Chase 5/24 count: The X1 card will appear on your credit report as a new account and so it will add to your 5/24 count.

Chase's 5/24 Rule: With most Chase credit cards, Chase will not approve your application if you have opened 5 or more cards with any bank in the past 24 months. To determine your 5/24 status, see: Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely.

Earning Rewards

2x Rewards

The X1 card can only be used to earn 2x.

3x Rewards

If you spend more than fifteen thousand dollars a year, you can get 3x everywhere.

A cap on 3x rewards has been imposed by X1.

Monthly Spending Limitation: The three (3) points per dollar will only be available on the first $7,500 of Eligible Spend each calendar month. All Eligible Spend in excess of $7,500 during the calendar month will earn two (2) points per dollar, even if the 3x Annual Spend Bonus has been activated.

4x, 5x, or 10x Rewards

There are two ways to earn rewards.

Upon startup: If you join X1 using a friend referral, you’ll earn a mystery bonus of 4x, 5x, or 10x on every dollar spent for the first 30 days.

Ongoing: For every friend you refer with an in-app invitation, you get 30 days of 4x, 5x, or 10x earnings.

4X or more via Boosts

You can earn up to 5x if you enroll in the X1 app.

Earn 4x Points on your next Amazon.com purchase

Earn 5x Points on your next Apple Pay purchase

Earn 5x Points on your next gas purchase

Earn 4x Points on your next restaurant purchase

Earn 4x Points on your next grocery purchase

Earn 200 More Points on your next $500+ purchase

Earn 400 More Points on your next $1,000+ purchase

You can earn a boost by using it before you make a purchase.

When I first signed up for the card, I picked an Apple Pay 5x boost and used it to buy a few items at the store, and then I used Apple Pay to pay at the pharmacy.

I immediately received an email confirming that the Boost worked. Subject: “Boost Completed: 5X Points Earned”. Content of email: “Merchant: CVS, Amount: $17.50, Total Points Earned: 87”.

Points showed up immediately in the X1 app. Most rewards programs wait until your statement closes before awarding points. In some cases (such as with Capital One, I believe), points are awarded once a purchase moves from pending to actual. In this case, the purchase was still pending.

I was immediately able to select a new Boost after the CVS purchase. Apple Pay 5x showed up again, so I picked it again. I thought that maybe it would always be available, but after using the Apple Pay Boost one or two more times, it was no longer an available option.

There is a bit of strategy involved in picking your boost, will my next purchase be with apple pay, or dining, or grocery, or online?

You can redeem for cash back for 0.7 cents per point value or you can offset purchases with specific merchants.

Redeeming Points for Eligible Purchases

The image above shows how I used points to offset American Airlines purchases

Points can be used to pay for items with a certain number of merchants.

Capital One has the ability to redeem miles for travel purchases and Chase has the ability to pay yourself back.

Open the X1 App and go to the Rewards tab (FYI: the Rewards Tab is labelled as either 2X, 3X, or 4X, depending upon your current earnings).

Select “Redeem” to see a list of eligible purchases from Rewards Partners that can be paid off with your Points

Choose an eligible Rewards Partner transaction and select “Pay Off”.

You must have enough Points available to redeem against the entire transaction amount (partial redemptions are not accepted).

The amount you paid with Points will be applied to the selected transaction as a statement credit and will reduce the outstanding balance on your account.

I erased several purchases and found that it worked as advertised.

If you redeem your points for charges with any of the merchants, you will get only 0.7 cents per point value.

Redeeming Points for Cash Back Statement Credit

Points can be redeemed for 0.7 cents each.

Earn 2x = 1.4% cash back (not good)

Earn 3x = 2.1% cash back (good)

Earn 4x = 2.8% cash back (excellent)

Risks

This section has not been updated in six months. You can ignore the part about X1 rolling out slowly now that it's public.

It may be a good thing that X1 is taking so long to roll out.

Several readers have told us that X1 has stopped them from using their rewards program after they opened the card.

I spent a good amount of money within the first days and posted my code in social media for people to skip the wait list, according to another reader. After some back and forth with customer support, he received a message saying, " hope you're well." I wanted to let you know that your account has been flagged for possible misuse of our rewards program, and that the team did a review of your account. We will have to close your account because of this.

It is necessary to connect the bank account where your salary is deposited so that X1 can determine your credit limit from that.

Regardless of how or why X1 has been shutting down accounts, the situation makes me nervous.

The card was used for a year.

Pros

No annual fee

No foreign transaction fees

No late payment fees (but you will be charged interest if your balance isn’t paid in full within 21 days of the close of each billing cycle)

High point earning rate (2x, 3x or more everywhere)

Awesome virtual card number features. I love using auto-expiring virtual cards to sign up for free trials without any risk of being charged when I forget to cancel.

Higher credit limit than most other cards

Cons

Unproven start-up. There’s a real risk to earning points with a start-up company. If they suddenly fold it is likely that you’ll lose all unredeemed points.

Shutdown risk. Early on, there were a number of reports of X1 shutting down people without any obvious reason. I don’t know if that’s still happening.

Possibly poor customer support. I haven’t had to deal with customer support so I can’t speak from experience, but several readers reported problems early on. It’s possible that these issues have since been corrected. I don’t know.

Rewards worth full value only if you shop with their qualifying merchants. If you want cash back, you’ll only get 0.7 cents per point.

No welcome bonus (unless you count the ability to earn 4x in the first month).

Adds to your 5/24 count

Chase's 5/24 Rule: With most Chase credit cards, Chase will not approve your application if you have opened 5 or more cards with any bank in the past 24 months. To determine your 5/24 status, see: Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely.

No hotel partners. As things stand today, you can redeem points at full value towards Hotels.com, Airbnb, and Vrbo, but I don’t see Marriott, Hyatt, IHG, Wyndham, Choice, or any other hotel brand on the list.

No transfer partners. Regular readers know that I love points that transfer to airline and hotel partners. X1 doesn’t offer this option.

The card earns 2x by default, 3x for those who spend 15k per year or more, and 4x for those who refer a friend.

2X: If you think that you’ll only earn 2x most of the time, then skip this card altogether and go with something like the Citi Double Cash to get a total of 2% cash back plus the option to transfer points to airline and hotel programs by adding the Citi Premier card to your collection in the future.

3X: If you’re sure you’ll spend $15K or more on the card each year and you’re unlikely to go over the monthly $7,500 cap, then X1 is worth considering. If you cash out your points for 0.7 cents each, the X1 becomes a 2.1% cash back card. That’s not bad. It’s possible to do better than that, but usually with big hoops involved. And if you’re interested in redeeming points against qualifying merchant charges, you’ll get 3% value from your X1 spend. That’s great.

4X or more: If you’re pretty sure that you can refer people regularly to the X1 card, then the X1 is a great option for you. Let’s assume that your normal earn rate will be 4x. If you cash out your points for 0.7 cents each, the X1 becomes a 2.8% cash back card while 4x earnings are in place. That’s excellent. And if you redeem for qualifying merchant charges, you’re looking at 4% value. That’s awesome.

It is possible to do better with other cards if you earn 2x, 3x, or more with the X1 card.

Bottom line

The X1 Card may not be ready for prime time with regards to customer support.

When I sign up for a free trial, I don't get charged even if I forget to cancel.

If you sign up for the best credit card offers you can earn more rewards than with the X1 card.